Midyear results 2017

Letter to shareholders

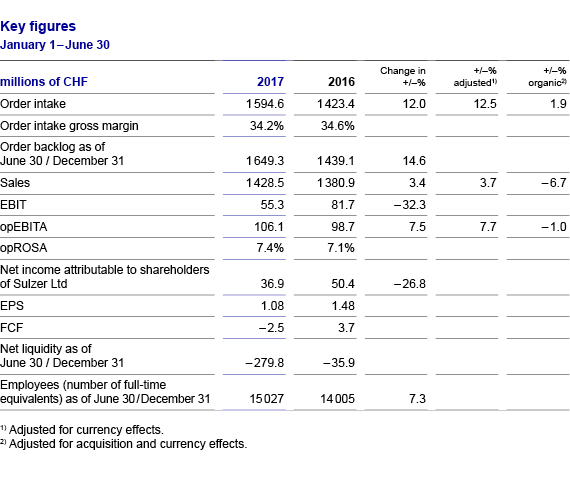

With the acquisitions we announced last year, we have laid the foundation for profitable growth in 2017. In the first half-year, our order intake increased by 12.5% compared with the same period of the previous year. Of this, 1.9% was organic and 10.6% through acquisitions. Let us briefly summarize the strategic rationale behind the acquisitions.

Peter Löscher, Chairman of the Board of Directors, and Greg Poux-Guillaume, CEO

"Our acquisition and sustained capital investments in a down market are laying the foundation for profitable growth."

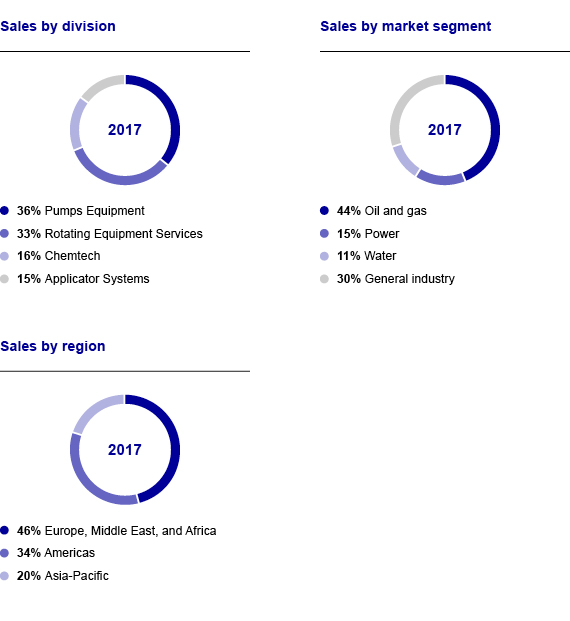

Our acquisition of the dispenser business PC Cox Group Ltd, closed in April 2016, allowed us to complete our product range for industrial adhesives. Through the acquisition of Geka, closed at the end of August 2016, we added a new, highly resilient market — beauty — to our portfolio. The development of the acquired businesses has exceeded our expectations. Together, PC Cox and Geka contributed CHF 99 million of order intake in the first half of 2017. As you know, we combined PC Cox, Geka, and Sulzer Mixpac Systems into a new division called Applicator Systems (APS) as of January 1, 2017. APS is active in resilient, high-margin end-market segments such as industrial adhesives, dental, healthcare, and beauty.

For our Pumps Equipment division we closed the acquisition of pumps manufacturer Ensival Moret (EM) at the end of January this year. EM is a good complement and added axial flow and slurry pump technologies to the Sulzer portfolio. It also strengthened market segments such as fertilizers, sugar, mining, and chemicals. Although EM’s profitability will only break even in 2017, we see significant sales synergies going forward. In the first half of this year, we reported an additional CHF 34 million of orders through EM.

In our service division, we closed the acquisition of Rotec GT at the end of June this year. The gas turbine service business, which focuses on the Russian market, significantly increased our presence in an important market for such services. Because of the requirements of the Russian market, it is of great value to have a large and local presence as an independent service provider. A total of CHF 17 million of order intake stems from Rotec.

A smaller but very promising acquisition is the Vessel Internal Electrostatic Coalescer (VIEC) technology, closed in January this year. This separation technology is going to be a winning upstream application as soon as the market rebounds. VIEC projects contributed CHF half a million of order intake since closing.

Taking further steps to grow and strengthen our businesses

In May, we signed a binding agreement to acquire Simcro. With that, we positioned ourselves in another new, attractive end-market segment — animal healthcare. Simcro is the market leader for veterinary devices such as injectors and applicators for livestock and companion animals. The acquisition not only helps us further diversify, it also enlarges our presence in New Zealand and Australia.

Putting together what belongs together

Apart from acquisitions, we changed our reporting structure for increased customer focus. We transferred our spare parts business for pumps from the Pumps Equipment (PE) to the Rotating Equipment Services (RES) division. This was the logical step in a development we started in previous years when we moved the pumps field service and workshops to RES. Our customers appreciate that they now have a single point of access for services and parts.

Talking about the Sulzer Full Potential (SFP) program, we are on track for the CHF 40 to 60 million of additional savings expected for the full year 2017. We also confirm our goal of cumulative savings of CHF 200 million for the full program from 2018 onwards. SFP has helped us counterbalance adverse market impacts in the past and will benefit our margins as soon as the market rebounds.

Performance in the first half of 2017

Order intake increased by 12.5% on a currency-adjusted basis and by 1.9% organically, i.e., adjusted for currency and acquisition effects. Orders from the oil and gas market stabilized on a low level with increased activity in the downstream market segment. Order intake in the power market went up thanks to Rotec’s contribution. Orders from the water market decreased because of fewer larger orders in the engineered water business. General industry grew driven by the acquisitions.

Sales increased by 3.7% on a currency-adjusted basis, whereas they decreased by 6.7% organically compared with the same period of the previous year. The organic decline is due to decreasing sales volumes from the oil and gas market in the Pumps Equipment division. Operational EBITA increased on a currency-adjusted basis and remained stable organically. Despite lower organic sales volumes, the operational EBITA margin (opROSA) increased to 7.4% from 7.1% in the first half of 2016.

Outlook

For the full year 2017, Sulzer is updating its guidance on order intake. The company previously communicated that order intake would grow by 5 to 8%. The updated guidance indicates that order intake is expected to grow by 7 to 10%. The company confirms its guidance on sales and operational EBITA margin. Sales are forecast to grow by 3 to 5%. OpROSA is expected to be around 8.5%.

Dear shareholders, we have seen our restructuring measures and acquisition strategy pay off in the first half-year 2017. We thank you for your support, especially in challenging times. We are looking forward to growing together with you.

Yours sincerely,

|

|

|

Peter Löscher |

Greg Poux-Guillaume |

EBIT: Operating income

opEBITA: Operating income before restructuring, amortization, impairments, and non-operational items

opROSA: Return on sales before restructuring, amortization, impairments, and non-operational items (opEBITA/sales)

EPS: Basic earnings per share

FCF: Free cash flow